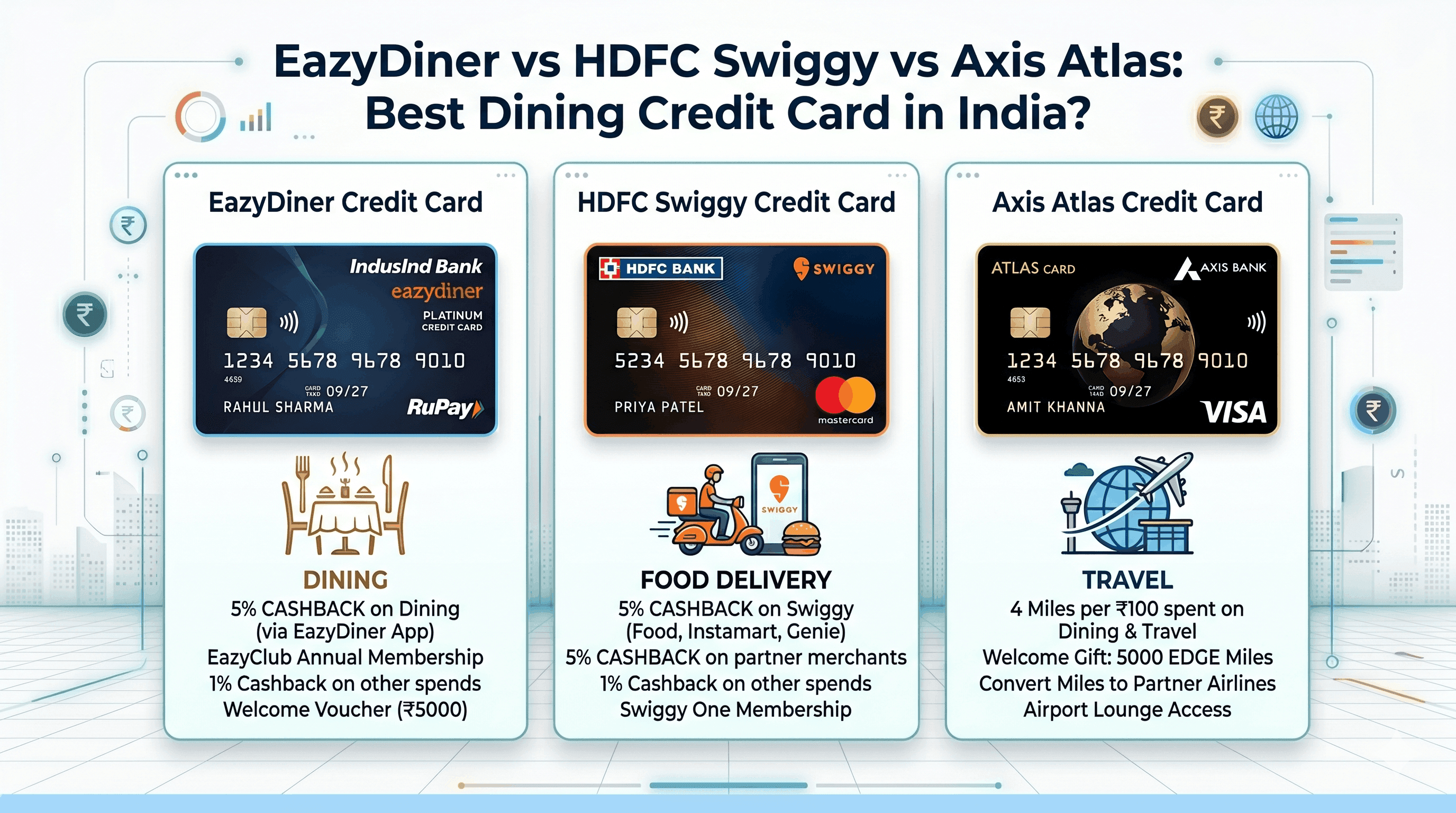

EazyDiner vs HDFC Swiggy vs Axis Atlas: Which Card Actually Saves You More in 2026?

By Satyapal Khakhal, Personal Finance Writer | Last Updated: May 2026

Satyapal Khakhal covers credit cards, personal finance, and investment products for Indian consumers. This comparison is based on publicly available card features from IndusInd Bank, HDFC Bank, and Axis Bank, cardholder reports from r/CreditCardsIndia, and comparison data from Paisabazaar, CardInsider, and CardExpert as of May 2026.

Here is something most comparison articles will not tell you upfront: one of the three cards in this comparison — the Axis Atlas — is no longer available to new applicants. Axis Bank quietly stopped accepting fresh applications in early 2026, with no press release and no official announcement. The card page still exists on their website, but the Apply Now button leads nowhere.

We are keeping it in this comparison for two reasons: hundreds of thousands of existing Atlas cardholders still use it daily, and understanding why it was considered the gold standard for dining and travel rewards helps explain what you are actually giving up — or gaining — with the two cards that are still available.

So: EazyDiner IndusInd vs HDFC Swiggy for new applicants in 2026. And where Atlas fits for those who already hold it. Here is the honest breakdown.

Quick Comparison: At a Glance

| Feature | EazyDiner IndusInd (Signature) | HDFC Swiggy (Original) | Axis Atlas (Closed) |

|---|---|---|---|

| Annual Fee | ₹2,999 + GST | ₹500 + GST | ₹5,000 + GST |

| Fee Waiver Threshold | Not publicly specified | ₹2 lakh annual spend | ₹15 lakh annual spend |

| Best Cashback Rate | 25–50% off dining (EazyDiner Prime) | 10% cashback on Swiggy (min ₹249/txn) | 5 EDGE Miles per ₹100 on travel |

| Base Earn Rate | 4 reward points per ₹100 | 1% cashback on all other spends | 2 EDGE Miles per ₹100 |

| Dining Benefit Type | Direct discount at restaurants | Cashback on Swiggy/Dineout orders | Travel miles, not dining-focused |

| Airport Lounge Access | 8 domestic visits/year (2/quarter) | None | Domestic + international |

| Movie Benefits | 2 free BookMyShow tickets/month (₹200 each) | None | None |

| Available to New Applicants? | ✅ Yes | ✅ Yes | ❌ No (closed early 2026) |

EazyDiner IndusInd Bank Credit Card — Built for People Who Actually Dine Out

The EazyDiner IndusInd Bank Signature Credit Card is the most focused dining card available in India right now. Its entire value proposition is built around the EazyDiner Prime membership it bundles — worth ₹2,495 annually — and the direct discount access that membership unlocks at over 2,000 partner restaurants across India.

The discount structure works like this: as a cardholder, you get a guaranteed 25% to 50% off at partner restaurants when you book and pay through the EazyDiner app using the PayEazy payment option. On top of this, there is an additional instant 25% discount (up to ₹1,000 per transaction) when you pay via PayEazy, capped at ₹2,000 per month for baseline spenders. If you spent ₹30,000 or more in non-dining transactions in the previous calendar month, the cap extends to ₹5,000 per month. Total maximum discount across both layers in a month: ₹5,000.

The reward earning structure runs separately from the discount: 10 reward points per ₹100 on dining, travel, shopping, and entertainment; 4 reward points per ₹100 on all other eligible spends except fuel. Each reward point is valued at ₹0.20, making the effective cashback rate 2% on high-earn categories and 0.8% on general spends.

Other Benefits Worth Noting:

- 8 complimentary domestic airport lounge visits per year (2 per quarter)

- 2 complimentary BookMyShow movie tickets per month (₹200 each, ₹400/month value)

- 1% fuel surcharge waiver on transactions between ₹400–₹4,000

- Postcard Hotels voucher worth ₹7,500 on card renewal

- Welcome benefit: 2,000 bonus EazyPoints on card activation

Where the EazyDiner Card Falls Short:

The 25% instant discount only applies when you pay through the EazyDiner app via PayEazy. Pay with the physical card at the table, use UPI, or use another payment method, and the instant discount does not apply — only the EazyDiner Prime membership discount remains. This is a significant operational constraint: you must remember to book through the app and complete payment through PayEazy every time, which is more friction than it sounds when you are at a restaurant table.

The card also has no international focus — no travel miles, no forex benefits, no hotel transfer partners. If you travel frequently, this card works best as a dedicated dining card alongside a separate travel card.

Annual fee: ₹2,999 + GST

Best for: Frequent restaurant diners in metro cities who will actively use the EazyDiner app booking flow

HDFC Swiggy Credit Card — High Cashback, Zero Complexity

The HDFC Swiggy Credit Card is the opposite of the EazyDiner in almost every way. Where EazyDiner rewards restaurant diners who book ahead and pay through a specific app, the Swiggy card rewards people who order food from their couch. The entire premise is cashback on Swiggy platform spends — food delivery, Instamart groceries, Genie, and Dineout bookings — with zero redemption complexity. Cashback is credited directly to the card statement.

The headline rate is 10% cashback on all Swiggy app spends, applicable from April 17, 2026 only on transactions of ₹249 or more per order. The monthly cashback cap across Swiggy spends is ₹1,500 per month — meaning you earn maximum cashback on approximately ₹15,000 of Swiggy spending per month. Beyond that cap, additional Swiggy spends earn at the base rate.

Beyond Swiggy, the card earns 5% cashback on select online shopping categories including Amazon, Flipkart, Myntra, Nykaa, Ajio, and BookMyShow (capped at ₹1,500/month on a minimum transaction of ₹100). All other eligible spends earn 1% cashback with a monthly cap of ₹1,000.

What the HDFC Swiggy Card Does Not Have:

No airport lounge access. No travel benefits. No international rewards. No dining discount at physical restaurants (Dineout covers online reservations only). A steep forex markup that makes it unsuitable for international transactions. This is a purely domestic, everyday cashback card — and at ₹500 annual fee with a ₹2 lakh spend waiver, it prices itself correctly for what it delivers.

One important 2026 update: HDFC has now launched two upgraded variants — the Swiggy HDFC ORNGE (₹500 fee, 5% cashback on Swiggy) and Swiggy HDFC BLCK (higher fee, 10% cashback with Swiggy BLCK membership). The original Swiggy HDFC card retains its 10% Swiggy cashback but with the new ₹249 minimum transaction requirement. Check the HDFC website for current variant availability and benefits.

Annual fee: ₹500 + GST (waived on ₹2 lakh annual spend)

Best for: Regular Swiggy users who order food delivery or groceries via Instamart multiple times per week

Axis Atlas — A Benchmark That Is No Longer Available

The Axis Atlas Credit Card closed to new applicants in early 2026. If you already hold one, your card continues to work, your EDGE Miles continue to accumulate, and your benefits remain intact for now. If you were planning to apply, you cannot.

We include it here because it set the standard for what a mid-range travel-with-dining card should look like, and comparing against it reveals the gaps in what the current market offers.

Atlas earned 5 EDGE Miles per ₹100 on travel, dining, and online spends (accelerated tier), and 2 EDGE Miles per ₹100 on all other eligible spends. At a typical redemption value of ₹0.25 per EDGE Mile when transferred to airline partners, this translated to approximately 1.25% cashback equivalent on general spends and 1.25–5% on accelerated categories — competitive but not exceptional.

Where Atlas genuinely stood out was in its gamified tier structure: cardholders who hit ₹3 lakh spend unlocked Silver status (enhanced lounge access), ₹7.5 lakh unlocked Gold status (better transfer ratios and milestone bonuses), and ₹15 lakh unlocked Platinum status. This spend-linked tier system incentivised consolidating all spending onto one card, and at higher tiers, the returns became genuinely strong.

For new applicants in 2026, the closest replacement for Atlas's travel rewards flexibility is the HSBC TravelOne (20 transfer partners at 1:1 ratios, ₹4,999 fee). For dining and lifestyle rewards, neither current card fully replicates what Atlas offered. EazyDiner comes closest for restaurant dining; HDFC Swiggy for delivery.

Annual fee: ₹5,000 + GST (waived on ₹15 lakh spend)

Available: Existing cardholders only. Not available for new applications as of 2026.

Real Savings Comparison: What Each Card Actually Delivers Per Month

Calculated for a typical Indian professional spending ₹10,000–₹15,000 per month on food and dining:

| Spend Scenario | EazyDiner IndusInd | HDFC Swiggy |

|---|---|---|

| ₹5,000/month dining out (2–3 restaurant visits) | ₹1,250–₹2,500 savings (25–50% discount via EazyDiner Prime) | ₹0 (card doesn't cover restaurant bill) |

| ₹5,000/month Swiggy/Instamart orders | Limited (no direct Swiggy cashback) | ₹500 cashback (10%, capped at ₹1,500/month) |

| ₹5,000/month online shopping | ₹100 cashback (4 pts/₹100 at ₹0.20/pt) | ₹250 cashback (5% on select partners) |

| Monthly movie tickets (2 shows) | ₹400 free (2 BookMyShow tickets) | ₹0 |

| Annual lounge visits (value at ~₹600/visit) | ₹4,800/year (8 visits) | ₹0 |

| Annual card cost (fee + GST) | ₹3,539 | ₹590 (or ₹0 if spend waiver met) |

The calculation matters because these cards serve different use cases. If you order Swiggy 3–4 times a week and rarely dine at restaurants, the Swiggy card at ₹500/year delivers 10% back with no effort. If you dine out at restaurants twice a week at mid-to-premium establishments, EazyDiner's direct discounts can save ₹1,500–₹2,500 per month — far exceeding the ₹3,539 annual cost in the first two or three months.

Which Card Should You Choose?

The honest answer depends entirely on one question: where does your food spending actually go?

If the majority of your food spend is at physical restaurants — you book tables, dine with colleagues or family, frequent mid-range to premium places in metros — the EazyDiner card's direct discount model will save you more in rupees, even accounting for the higher annual fee. The condition is that you use the EazyDiner app booking flow religiously. If you skip the app and pay directly, the card's primary benefit disappears.

If the majority of your food spend is through delivery apps, home cooking with groceries, or ordering from Swiggy multiple times a week — and you want zero redemption complexity and a near-free card — the HDFC Swiggy card is the cleaner choice. The 10% cashback lands directly on your statement with no points systems, no partner transfers, no expiry tracking.

If you hold an existing Axis Atlas, there is no urgent reason to close it. Your existing EDGE Miles balance remains valid, your tier benefits continue, and many Atlas holders are being offered upgrades to Axis Magnus via their relationship managers. Hold it, use it, and monitor Axis's communications for any changes.

The Common Mistake That Costs Most Cardholders Money

Most people choose credit cards the way they choose phones — based on what their friends have or what they saw advertised. The EazyDiner card is prominently marketed. The Swiggy card has Swiggy's brand behind it. Neither of these is a reason to apply.

The costly mistake is applying for the EazyDiner card when 70% of your food spend is delivery orders — and applying for the Swiggy card when you primarily dine at restaurants. In both cases, the card's headline benefit is irrelevant to your actual lifestyle, and you end up paying an annual fee for benefits you never use.

Spend two minutes reviewing your last three months of UPI statements before applying. The split between restaurant spends and delivery app spends will tell you which card wins for your situation without any further analysis.

Honest Verdict

Neither card is universally better. They are built for different versions of the same lifestyle.

The EazyDiner IndusInd Signature is the better card for the higher-spending restaurant diner who will actively use the EazyDiner booking ecosystem. At ₹2,999/year, it pays for itself in one or two good restaurant evenings per month for someone who consistently uses the discount mechanism. The lounge access and movie tickets add meaningful secondary value. Its weakness is operational friction — you must remember to use the app every single time.

The HDFC Swiggy is the better card for frequent delivery users who want high cashback with zero effort. At effectively ₹0/year (once the ₹2 lakh spend waiver is met), the value-to-fee ratio is exceptional for its target user. Its weakness is narrow scope — outside of Swiggy and selected online categories, the card offers little.

EazyDiner Rating: 3.8/5 — Strong for its target user, high operational dependency

HDFC Swiggy Rating: 4.2/5 — Outstanding value-to-fee ratio for Swiggy-heavy households

Frequently Asked Questions

Is the Axis Atlas credit card still available in 2026?

No. Axis Bank stopped accepting new applications for the Atlas Credit Card in early 2026. The closure was not formally announced — the card page remains live on Axis's website, but applications are no longer processed. Existing cardholders retain their benefits, EDGE Miles, and lounge access until Axis communicates otherwise. The closest alternative for new applicants is the HSBC TravelOne for travel rewards, or the EazyDiner IndusInd card for dining.

Does the EazyDiner discount apply automatically when I pay with the card?

No, and this is the most important thing to understand before applying. The additional 25% instant discount (up to ₹1,000 per transaction) only applies when you book through the EazyDiner app and pay via the PayEazy option within the app. If you pay with the physical card at the restaurant, via UPI, or through any other method, the instant discount does not apply. The EazyDiner Prime membership discount (25–50%) still applies through the app booking process, but the extra layer of discount requires the PayEazy payment flow.

What is the monthly cashback cap on the HDFC Swiggy card?

As of May 2026, the 10% cashback on Swiggy spends (food delivery, Instamart, Genie, Dineout) is capped at ₹1,500 per month and requires a minimum transaction of ₹249 per order (effective from April 17, 2026). The 5% cashback on select online shopping categories is separately capped at ₹1,500 per month. The 1% base cashback on all other spends is capped at ₹1,000 per month. Check HDFC Bank's website for current terms as cashback structures can change.

Can I hold both the EazyDiner and HDFC Swiggy card at the same time?

Yes, and for many households this is actually the optimal strategy. EazyDiner for restaurant visits, HDFC Swiggy for delivery orders. The combined annual fee is approximately ₹3,539 + ₹590 = ₹4,129, which most active users in both categories would recover within two months of regular use.

Which card is better for someone who uses Swiggy Dineout?

The HDFC Swiggy card earns 10% cashback on Swiggy Dineout bookings as part of its Swiggy platform cashback (capped at ₹1,500/month combined across all Swiggy spends). The EazyDiner card offers direct discounts at physical restaurants through its Prime membership, but Dineout and EazyDiner are competing platforms — EazyDiner Prime benefits do not apply to Swiggy Dineout bookings. If you use Swiggy Dineout specifically, the HDFC Swiggy card is the better fit.

What should existing Axis Atlas cardholders do in 2026?

Hold your card and do not cancel. Your existing EDGE Miles balance remains valid (miles expire 3 years from earning date — check your Axis app). Your benefits are unchanged. Many Atlas cardholders are being offered upgrades to the Axis Magnus through their relationship managers, particularly those with Burgundy accounts. Contact your Axis RM or customer care to check upgrade eligibility if you want to move to a higher-tier card within the Axis ecosystem.

Related reading: Best Credit Cards in India 2026 | HSBC TravelOne Review 2026

Disclaimer: This comparison is for informational purposes only and does not constitute financial advice. Credit card features, fees, cashback rates, and eligibility criteria are subject to change by IndusInd Bank and HDFC Bank at any time without prior notice. Information in this article is based on publicly available data as of May 2026. Verify all current terms directly on the official IndusInd Bank and HDFC Bank websites before applying. gpaisa.in is not affiliated with any card issuer and does not receive compensation for this comparison.