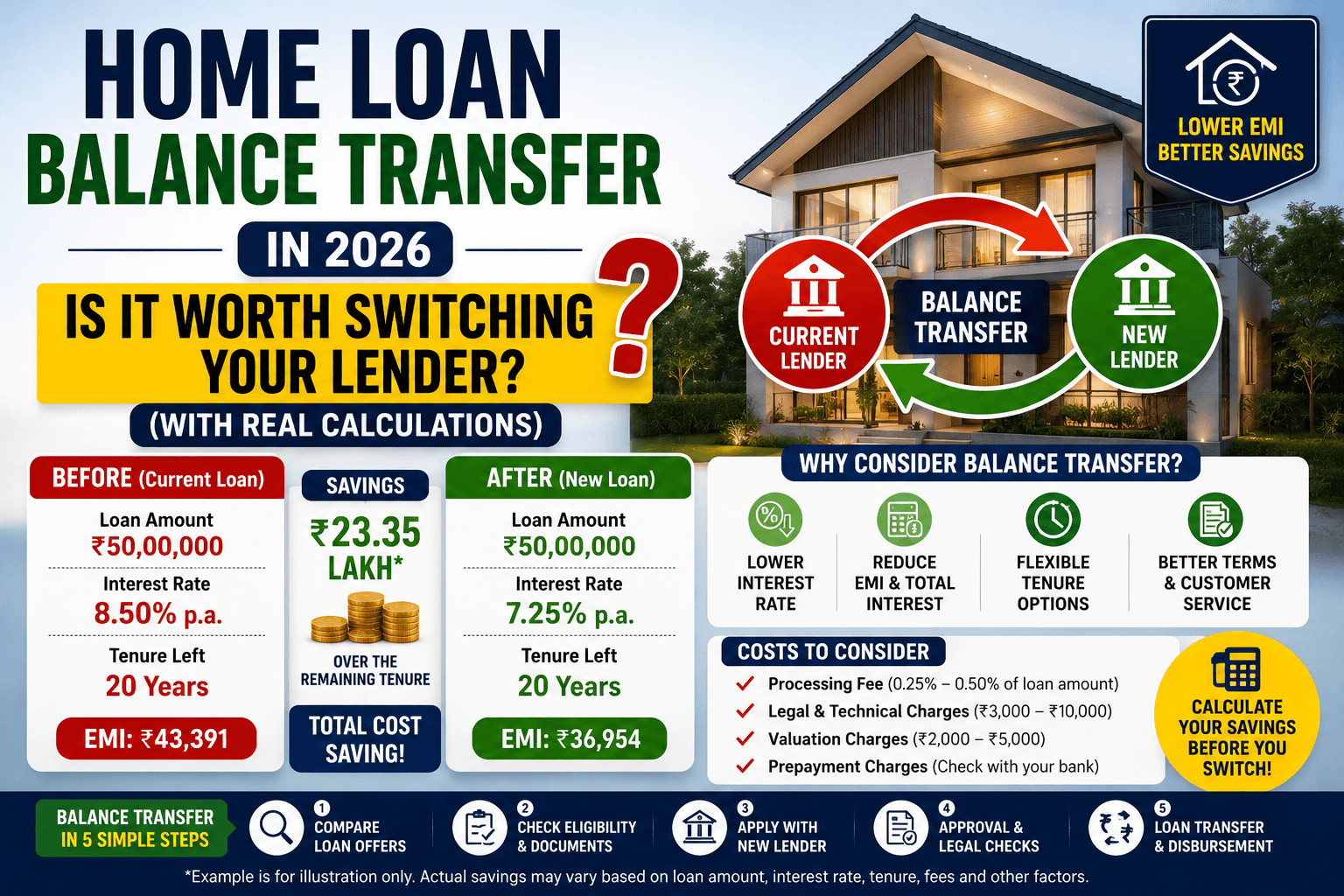

Home Loan Balance Transfer in 2026: Is It Worth Switching Your Lender?

By Satyapal Khakhal, Personal Finance Writer

Home loan rate data sourced from SBI, HDFC, ICICI, Axis, and Kotak official websites as of May 2026. Transfer cost calculations based on standard processing fee structures and stamp duty requirements. All EMI figures calculated using standard amortisation formula. Use gpaisa.in's home loan calculator for your specific figures. This article is for informational purposes only. gpaisa.in is not registered with SEBI.

With SBI's home loan rate now starting at 8.50% and the RBI having cut rates by 125 basis points since February 2025, many borrowers who took loans at 9.25–9.75% in 2023–24 are sitting on a rate that is 0.75–1.25% higher than what a new borrower would pay today. The natural question follows: should I transfer my home loan to a lender offering a lower rate?

The answer is not always yes — and the decision is more nuanced than simply comparing your current rate to the market rate. A balance transfer involves real costs — processing fees, legal charges, stamp duty on the new mortgage, and the time cost of the paperwork — that need to be offset by the interest savings before the transfer makes financial sense.

This article gives you the exact calculation to make this decision for your specific loan, the current best rates available for transfers in 2026, and the step-by-step process so you know what you are getting into before you start.

What Is a Home Loan Balance Transfer?

A home loan balance transfer — also called a home loan refinance — is the process of moving your outstanding home loan from your current lender to a new lender, typically to get a lower interest rate. The new lender pays off your outstanding principal to the old lender, and you begin repaying the new lender at the new (lower) rate.

The key distinction from a regular prepayment: in a balance transfer, only the outstanding principal moves — not the original loan amount. If you borrowed ₹60 lakh 3 years ago and have repaid ₹8 lakh of principal, only the remaining ₹52 lakh transfers to the new lender.

Balance transfers are available from virtually all major banks and housing finance companies (HFCs). Most lenders actively market balance transfer offers because acquiring an existing borrower with a clean repayment track record is lower risk than approving a new borrower.

When Does a Balance Transfer Actually Make Sense? The Break-Even Calculation

The decision framework is straightforward: a balance transfer makes financial sense when the total interest saved over the remaining loan tenure exceeds the total cost of the transfer. The point at which savings equal costs is the break-even point — and you need to plan to stay in the loan beyond that point for the transfer to be worthwhile.

Here is the calculation structure:

| Step | What to calculate |

|---|---|

| Step 1 | Calculate your current EMI and total interest remaining at current rate |

| Step 2 | Calculate new EMI and total interest at the new rate (same outstanding principal, same remaining tenure) |

| Step 3 | Calculate monthly EMI saving (current EMI minus new EMI) |

| Step 4 | Calculate total transfer cost (processing fee + legal charges + stamp duty + valuation fee) |

| Step 5 | Divide total cost by monthly saving = break-even in months |

| Step 6 | If you plan to continue the loan beyond the break-even period, the transfer is worth it |

Real Calculations: Four Loan Scenarios in 2026

The following examples use a transfer from a typical 2023–24 rate of 9.25% to SBI's current starting rate of 8.50% — a difference of 0.75%. This is a realistic scenario for many borrowers who took loans 18–24 months ago and have not yet benefited from RBI's rate cuts due to MCLR-linked loans or slow transmission.

Scenario 1: ₹40 lakh outstanding, 18 years remaining

| Current loan (9.25%) | After transfer (8.50%) | |

|---|---|---|

| Outstanding principal | ₹40,00,000 | ₹40,00,000 |

| Monthly EMI | ₹36,895 | ₹35,083 |

| Monthly saving | ₹1,812/month | |

| Total interest remaining | ₹39,72,420 | ₹35,77,788 |

| Total interest saved | ₹3,94,632 | |

| Estimated transfer cost | ₹40,000–₹55,000 | |

| Break-even period | 22–30 months | |

| Verdict | ✅ Worth it — 16 years remain after break-even | |

Scenario 2: ₹60 lakh outstanding, 20 years remaining

| Current loan (9.25%) | After transfer (8.50%) | |

|---|---|---|

| Outstanding principal | ₹60,00,000 | ₹60,00,000 |

| Monthly EMI | ₹55,343 | ₹52,123 |

| Monthly saving | ₹3,220/month | |

| Total interest remaining | ₹72,82,320 | ₹65,09,520 |

| Total interest saved | ₹7,72,800 | |

| Estimated transfer cost | ₹55,000–₹75,000 | |

| Break-even period | 17–23 months | |

| Verdict | ✅ Strongly worth it — ₹7+ lakh in savings | |

Scenario 3: ₹25 lakh outstanding, 7 years remaining

| Current loan (9.25%) | After transfer (8.50%) | |

|---|---|---|

| Outstanding principal | ₹25,00,000 | ₹25,00,000 |

| Monthly EMI | ₹40,126 | ₹39,396 |

| Monthly saving | ₹730/month | |

| Total interest remaining | ₹8,70,576 | ₹8,09,232 |

| Total interest saved | ₹61,344 | |

| Estimated transfer cost | ₹30,000–₹45,000 | |

| Break-even period | 41–62 months | |

| Verdict | ⚠️ Marginal — only 84 months remain after transfer costs; barely worth it | |

Scenario 4: ₹70 lakh outstanding, 25 years remaining, 1% rate difference

| Current loan (9.50%) | After transfer (8.50%) | |

|---|---|---|

| Outstanding principal | ₹70,00,000 | ₹70,00,000 |

| Monthly EMI | ₹61,066 | ₹56,204 |

| Monthly saving | ₹4,862/month | |

| Total interest remaining | ₹1,13,19,800 | ₹98,61,200 |

| Total interest saved | ₹14,58,600 | |

| Estimated transfer cost | ₹65,000–₹90,000 | |

| Break-even period | 13–19 months | |

| Verdict | ✅ Absolutely worth it — ₹14.5 lakh in lifetime savings | |

All EMI calculations at quoted rates for given outstanding and tenure. Transfer costs are estimates — actual costs vary by lender and state. Use gpaisa.in's Home Loan Calculator for your exact figures.

The clear pattern from these four scenarios: Balance transfers are most compelling when the outstanding principal is large (₹50 lakh+), the remaining tenure is long (15+ years), and the rate difference is at least 0.50%. As outstanding principal or remaining tenure shrinks, the transfer becomes progressively less worth the effort and cost.

Complete Cost of a Home Loan Balance Transfer in 2026

Many borrowers focus only on the processing fee and underestimate the full cost of a transfer. Here is every cost you will encounter:

| Cost component | Typical amount | Notes |

|---|---|---|

| Processing fee (new lender) | 0.5–1% of loan amount or ₹5,000–₹15,000 flat | Most banks cap at ₹10,000–₹15,000 for transfers |

| Legal and technical fee | ₹5,000–₹15,000 | New lender's lawyer verifies title documents |

| Stamp duty on new mortgage | 0.1–0.5% of loan amount (state-dependent) | Maharashtra: 0.3%, Delhi: 0.5%, Karnataka: 0.5% |

| Property valuation fee | ₹2,500–₹5,000 | New lender revalues the property |

| Foreclosure charges (old lender) | Nil for floating rate loans (RBI mandate) | Fixed rate loans may charge 2–4% of outstanding |

| NOC and document retrieval charges | ₹0–₹2,000 | Many banks charge for issuing NOC letter |

| Total estimated cost | ₹30,000–₹90,000 | Depends on loan size, state, and lender |

Important note on foreclosure charges: RBI mandates that banks cannot charge foreclosure penalties on floating rate home loans taken by individual borrowers. If your current lender is quoting a foreclosure charge on a floating rate loan, this is incorrect — you can escalate to RBI's Banking Ombudsman. Fixed rate loans are exempt from this rule and may carry 2–4% prepayment penalties, which significantly changes the transfer math.

Best Banks for Home Loan Balance Transfer in June 2026

Not all lenders compete equally on balance transfers. Some offer special transfer rates lower than their standard rates to attract well-seasoned borrowers with clean repayment history:

| Bank | Balance transfer rate | Processing fee | Key condition |

|---|---|---|---|

| SBI | 8.50%–9.15% | Nil (limited period offer, verify) | CIBIL 700+ required, clean 12-month repayment history |

| HDFC Bank | 8.75%–9.40% | ₹3,000–₹10,000 | CIBIL 750+ preferred for best rate |

| Axis Bank | 8.75%–9.30% | ₹5,000–₹10,000 | Salary account relationship helps |

| Kotak Mahindra | 8.75%–9.25% | ₹10,000 flat | Self-employed borrowers also eligible |

| PNB Housing Finance | 8.60%–9.50% | 0.5% or max ₹15,000 | HFC — may have faster processing |

| ICICI Bank | 8.75%–9.40% | ₹3,500 upwards | Existing ICICI customers get preferential terms |

| Bank of Baroda | 8.50%–9.15% | Nil to ₹10,000 | Competitive for government employees |

Rates as of May 2026. These are starting rates for salaried applicants with CIBIL 750+. Verify current transfer-specific offers on official bank websites before applying — transfer offers change frequently and banks periodically run zero-processing-fee campaigns.

Negotiation tip: Before approaching a new lender, tell your existing lender you are considering a transfer and ask them to match the external rate. Many lenders — particularly private banks — will reduce your rate by 25–50 basis points to retain you, at zero transfer cost. A retention rate reduction from your existing bank is almost always better than a transfer because it costs nothing and involves no paperwork. Always try this first.

The MCLR vs EBLR Factor: Why Many Borrowers Are Stuck at High Rates

A significant number of home loan borrowers who took loans before October 2019 are still on MCLR (Marginal Cost of Lending Rate) based pricing. Loans taken after October 2019 are mandatorily linked to an external benchmark — typically the repo rate — under RBI's EBLR framework.

The difference matters enormously in a rate cut cycle:

- EBLR loans: Rate resets within 3 months of any repo rate change. A borrower on EBLR should have seen rates fall by the full 125 basis points since February 2025.

- MCLR loans: Rate resets based on the bank's own cost of funds, which moves slower than the repo rate. MCLR-linked borrowers typically see only 40–70% of repo rate cuts transmitted to their loan rate.

If you are on MCLR and your rate has not fallen significantly despite 125 bps of RBI cuts, you have two options: request a switch from MCLR to EBLR within your current bank (typically ₹2,000–₹5,000 switching fee, sometimes nil), or do a full balance transfer to a new bank at EBLR-linked rates. The internal switch is almost always cheaper and faster than a full transfer — do this first if your bank offers it.

Step-by-Step: How to Actually Do a Home Loan Balance Transfer

Step 1 — Check your current loan terms (1–2 days)

Get your latest home loan statement showing outstanding principal, current interest rate, remaining tenure, and rate type (MCLR/EBLR/fixed). This is your baseline for comparison.

Step 2 — Try the retention approach first (1 week)

Call your bank's home loan department and ask for a rate reduction citing market rates. Follow up in writing. If they agree to reduce by 0.25–0.50% within your existing bank, this is the cheapest outcome — no transfer costs, no paperwork.

Step 3 — Get quotes from 2–3 new lenders (1 week)

Approach SBI, HDFC, and Axis (or whichever banks you prefer) with your outstanding amount, remaining tenure, and repayment track record. Ask specifically for their balance transfer rate and all associated costs. Get this in writing — verbal quotes are not reliable.

Step 4 — Run the break-even calculation (1 day)

Using the quotes received, calculate: total interest saved (current rate vs new rate, same outstanding and tenure) minus total transfer costs = net saving. Divide total cost by monthly EMI saving to get break-even in months. Proceed only if break-even is well within your remaining tenure.

Step 5 — Submit documents to new lender (1–2 weeks)

Standard documents required:

- KYC documents (Aadhaar, PAN, passport-size photos)

- Last 6 months bank statements

- Last 3 months salary slips (salaried) or last 2 years ITR (self-employed)

- Existing home loan account statement (last 12 months)

- Property documents (title deed, sale agreement, approved plan)

- Latest property tax receipt

Step 6 — New lender sanction and foreclosure letter (2–4 weeks)

Once the new lender approves your transfer, they issue a sanction letter. You then apply to your existing lender for a foreclosure letter — a document stating the exact outstanding amount as of a specific date and confirming there are no pending dues. This typically takes 7–14 days and may involve a small administrative fee.

Step 7 — New lender pays off old lender (1–2 weeks)

The new lender issues a demand draft or bank transfer to your old lender for the outstanding amount. Your old loan closes. Your original property documents (title deed, sale agreement) are released from the old lender's custody and handed over to the new lender.

Step 8 — Register new mortgage (1 week)

The new mortgage (equitable or registered) is created in favour of the new lender. This involves stamp duty payment and in some states, a visit to the sub-registrar's office. This step is often handled by the new lender's legal team.

Total timeline: 6–10 weeks from decision to completion. This is the real time cost of a balance transfer. If you need to close the loan quickly for any reason during this period, the process can create complications.

Who Should Do a Balance Transfer Right Now — And Who Should Not

Transfer makes clear sense if:

- Your current rate is 9.0% or above and the market offers 8.50–8.75%

- Outstanding principal is above ₹40 lakh

- Remaining tenure is 12+ years

- Your repayment record is clean for the last 12 months

- Your CIBIL score is 700+ (750+ for best rates)

- Your income situation is stable and you can provide current employment documents

Transfer is not worth it if:

- Remaining tenure is below 7 years — interest savings are too small to justify costs

- Rate difference is below 0.40% — break-even period will exceed 4+ years

- You have a fixed rate loan with a prepayment penalty — penalty may exceed savings

- Your CIBIL score has dropped below 700 since taking the original loan — you may not qualify for the best transfer rates and could end up with a worse deal

- You are already getting the benefit of rate cuts through your EBLR-linked loan — your current rate may already be at market

- You are planning to sell the property or prepay fully within 3 years — break-even will not be reached

Top-Up Loan During Balance Transfer: A Hidden Benefit

One frequently overlooked advantage of a balance transfer is the ability to take a top-up loan simultaneously. When you transfer your home loan, the new lender assesses your property value fresh. If your property has appreciated since you took the original loan — which is likely given Indian real estate trends since 2021 — the new lender may offer a higher loan-to-value, allowing you to borrow an additional amount above the outstanding balance.

This top-up is disbursed at home loan interest rates (8.50–9.0%), which is significantly cheaper than a personal loan (11–14%) or a loan against property (9.5–12%). If you have a home renovation planned, a large expense coming, or any other financial need, a balance transfer top-up can provide funds at the lowest rate available to retail borrowers.

The tax treatment of the top-up depends on usage: if used for property purchase or construction, interest qualifies for Section 24(b) deduction; if used for renovation, the old Section 24(b) limit applies; if used for personal expenses, no deduction is available.

Calculate Your Exact Savings

Every number in this article is based on illustrative scenarios. Your actual saving depends on your specific outstanding balance, remaining tenure, current rate, and the transfer rate you qualify for based on your credit profile.

Use gpaisa.in's Home Loan Calculator to:

- Calculate your current EMI and total interest remaining at your current rate

- Recalculate with the transfer rate to see the new EMI and total interest

- See the year-wise amortisation schedule showing exactly how much interest you pay each year

- Compare multiple rate scenarios side by side

Frequently Asked Questions

Is home loan balance transfer worth it in 2026?

For borrowers with ₹40 lakh+ outstanding, 12+ years remaining, and a current rate of 9.0% or above, yes — transferring to current market rates of 8.50–8.75% saves ₹3–15 lakh in total interest depending on loan size. For smaller loans or shorter remaining tenures, the transfer costs may outweigh the savings. Calculate your break-even point before deciding.

What is the minimum rate difference for a home loan balance transfer to be worth it?

As a rule of thumb, a rate difference of at least 0.50% is generally required for a balance transfer to make financial sense after accounting for all transfer costs. Below 0.50%, the break-even period stretches beyond 5 years on most loan sizes. At 0.75% or more, the transfer almost always pays off quickly.

Does a home loan balance transfer affect CIBIL score?

Yes, in two ways. First, the new lender makes a hard enquiry on your CIBIL report when you apply, temporarily reducing your score by 5–10 points. Second, your old loan account is closed (a positive closed account) and a new loan account is opened. The net effect on your CIBIL score is typically neutral to mildly positive after 3–6 months of regular payments on the new loan.

Can I do a home loan balance transfer if I have missed EMIs?

Most lenders require a clean repayment record of at least 12 months for a balance transfer. One or two minor delays (reported as DPD 30 but not NPA) may be overlooked depending on the lender, but any default or NPA status in recent history will result in rejection from most banks. Some NBFCs and smaller HFCs may consider borrowers with imperfect histories at higher rates.

How long does a home loan balance transfer take?

The complete process — from deciding to transfer to the new loan becoming active — typically takes 6–10 weeks. Key steps: new lender approval (2–3 weeks), foreclosure letter from old lender (1–2 weeks), fund transfer and document handover (1–2 weeks), new mortgage registration (1 week). Delays in document collection or legal verification can extend this timeline.

My bank reduced my rate slightly — should I still transfer?

Rerun the calculation with your bank's offered reduced rate. If the difference between the reduced rate and the best transfer rate is now below 0.40%, the transfer probably does not pay off after costs. If the difference is still 0.50%+ and you have significant outstanding and tenure remaining, the transfer may still be worth it. The internal retention offer saves time and cost but should not automatically stop you from seeking a genuinely better rate externally.

Use our calculator: Home Loan EMI Calculator — gpaisa.in | Related reading: Home Loan vs Rent in India 2026 | RBI Repo Rate 2026 — Impact on EMI and FD | How to Improve Your CIBIL Score

Disclaimer: Home loan interest rates, processing fees, and transfer terms are subject to change by lenders at any time. All calculations in this article are illustrative based on rates and costs as of May 2026. This article is for informational and educational purposes only and does not constitute financial or legal advice. Please verify all current rates and terms directly with lenders before initiating a balance transfer. gpaisa.in is not registered with SEBI. Consult a SEBI-registered financial advisor before making significant financial decisions.