Alpine Texworld IPO 2026: GMP, Subscription, Full Review & Should You Apply?

By Satyapal Khakhal

Not every IPO that lands in the middle of a busy week deserves your money — and Alpine Texworld is shaping up to be exactly the kind of issue that needs a second, harder look before you tap "apply." On paper it's a growing textile manufacturer with a green-energy angle. But dig into the grey market and the subscription numbers, and a more cautious story appears. Here's the full, no-spin breakdown.

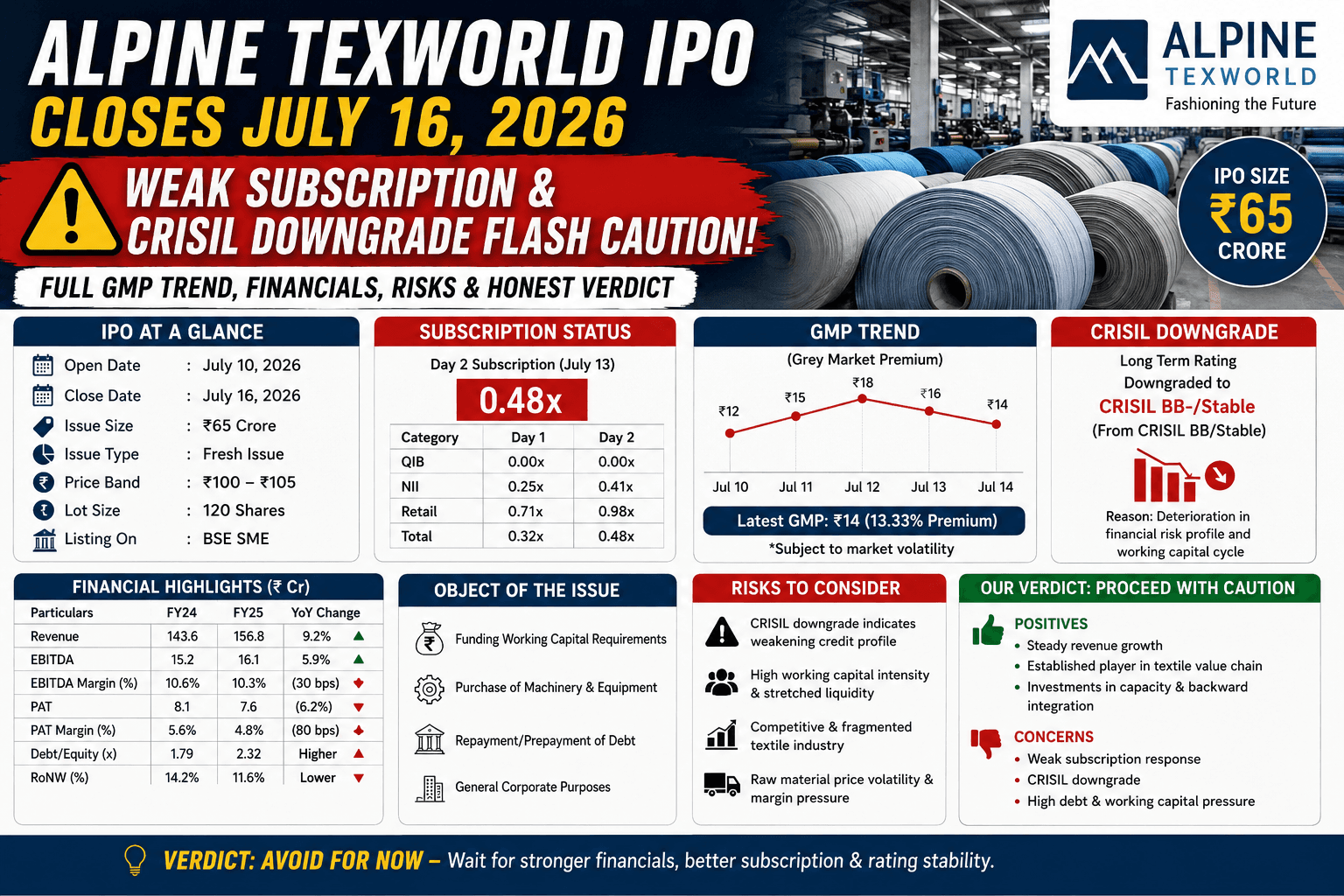

Alpine Texworld IPO: Key Details at a Glance

The IPO opened for subscription on July 14, 2026 and closes on July 16, 2026. The price band is fixed at ₹100 to ₹105 per share, with a lot size of 142 shares — meaning a minimum retail investment of ₹14,910 at the upper band. It's a mainboard issue aiming to raise ₹126.25 crore through a 100% fresh issue of 1.20 crore equity shares.

Allotment is expected to be finalised on July 17, with shares tentatively listing on both the NSE and BSE on July 21, 2026. D&A Financial Services is the book-running lead manager, and KFin Technologies is the registrar. Notably, promoter holding will fall from 90.36% to about 61.96% after listing.

Here's the snapshot: IPO opens July 14 and closes July 16, 2026; price band ₹100–₹105; face value ₹10; lot size 142 shares; minimum investment ₹14,910; total issue ₹126.25 crore (100% fresh issue); allotment July 17; listing July 21, 2026 on NSE and BSE; lead manager D&A Financial Services; registrar KFin Technologies.

What Does Alpine Texworld Actually Do?

Incorporated in February 2016, Alpine Texworld is a Gujarat-based textile company engaged in dyeing, processing and finishing fabrics, along with yarn manufacturing and sizing services. It runs two manufacturing units with an annual installed capacity of around 6,000 MT of cotton and blended yarn, and operates 112 high-speed looms that produce denim, suiting, shirting and ready-for-dyeing (RFD) fabrics for garment makers and textile traders.

Its more distinctive feature is the push into renewable energy. Because electricity is one of the biggest costs in textile processing, the company commissioned an 820 kW rooftop solar plant in January 2024 and a larger 5.4 MW ground-mounted solar project in Banaskantha in March 2025. The idea is simple: cut power bills, improve margins, and tick the sustainability box that export buyers increasingly care about. As of March 31, 2026, the company employed 164 people.

Where the Money Goes

Because this is a 100% fresh issue, all the proceeds flow into the company rather than to exiting shareholders — a genuine positive. The funds are earmarked for setting up a new weaving unit (proposed Manufacturing Unit 3) in Ahmedabad to expand grey fabric production, along with debt reduction and general corporate purposes. If executed well, this could expand capacity and strengthen a stretched balance sheet.

GMP Report: What the Grey Market Is Signalling

This is the part worth slowing down on, because the grey market premium (GMP) here has been weak and choppy rather than confident. The trend tells the story: GMP sat at ₹0 on July 9, rose to about ₹2 between July 10 and 12, improved to ₹5 on July 13 and 14, then climbed to ₹10 on July 15 (an implied listing gain of roughly 9.5%).

At the latest GMP of ₹10, the estimated listing price works out to around ₹115 against the ₹105 upper band. The direction is improving, which is encouraging — but the fact that it started at zero just days earlier tells you this is thin, speculative activity, not broad conviction.

A reminder that always bears repeating: GMP is an unofficial, unregulated indicator that changes daily with sentiment. It is not a prediction of the actual listing price, and it should never be the sole basis for an investment decision.

Subscription Status: The Bigger Warning Sign

If the GMP is merely lukewarm, the subscription numbers are the real concern. Two days into the three-day window (as of July 15), demand was soft: overall subscription was just 0.48 times, with QIBs at 1.00x, retail investors at 0.50x, and non-institutional investors at 0.41x.

An issue that is still under-subscribed — below 1x — this late in its window is a meaningful red flag. It means that, at this stage, there simply aren't enough bids to fill the offer. The odd combination of a rising GMP alongside weak subscription usually points to thin grey-market speculation rather than genuine, broad-based demand.

Financials: Genuinely Mixed Signals

Here's where you need to read carefully, because the reported picture is not clean. Some coverage highlights a strong FY26, with revenue up around 47% year-on-year and net profit surging about 152%. Yet other analysis cautions that revenue and profit actually declined in FY26 versus FY25, and that the company's earnings per share sits below its listed peers.

Whichever framing proves more accurate, the takeaway is the same: this is not a clean, unambiguous growth story you can buy on autopilot. When the financial narrative itself is contested, the burden shifts to valuation — and that's where Alpine struggles.

The Risks You Can't Ignore

Aggressive valuation. Multiple independent reviews have flagged the pricing as steep. One analyst was blunt: the FY26 margins look surprisingly high for a business in such a competitive, fragmented segment, the issue appears aggressively priced, and skipping this "pricey and dicey" IPO would do no harm. When a company's margins outpace peers in a commoditised industry, the market's first instinct is scepticism about whether those margins are sustainable.

A fresh credit-rating downgrade. Alpine enters the market carrying elevated borrowings and a recent CRISIL downgrade to BB/Stable — a rating that signals higher credit risk. For a capital-intensive manufacturer, that's not a footnote; it's central to the investment case.

Concentration and competition. The company also faces customer and geographic concentration, and operates in one of India's most fragmented, price-competitive industries, where pricing power is limited and larger players enjoy scale advantages.

Strengths, To Be Fair

There are positives worth acknowledging: a genuine, partially integrated manufacturing business spanning yarn, sizing and weaving; modern automated machinery from established global makers; meaningful renewable-energy investment that lowers power costs and aids export appeal; a 100% fresh issue, so proceeds fund growth rather than an owner's exit; and exposure to India's large and growing textile sector.

Should You Apply? My Honest Verdict

Weighing everything, this one leans clearly toward avoid or skip — particularly if you're chasing listing gains.

The deciding factor is the weak demand. An IPO under-subscribed at 0.48x on Day 2 typically points to a muted or flat listing, which makes the ~9.5% GMP-implied gain look optimistic. Layer on a valuation that several analysts independently call aggressive, a fresh CRISIL downgrade to BB/Stable, and a contested financial picture with below-peer EPS, and the risk-reward simply isn't attractive for most investors.

The only investors who might reasonably consider it are those with a genuine long-term conviction in the vertical-integration and solar-cost story — and even they should read the Red Herring Prospectus closely, weigh the debt and downgrade, and size any application small.

One practical tip: subscription can jump on the final day, especially in the QIB and NII buckets. If you're undecided, the smartest move is to watch the final-day subscription figures before the window closes. A late surge comfortably above 1x would soften — though not erase — the demand concern.

Frequently Asked Questions (FAQs)

What is the Alpine Texworld IPO GMP today? As of July 15, 2026, the grey market premium was around ₹10, implying a possible listing gain of roughly 9.5% over the ₹105 upper band. It had been as low as ₹0 on July 9. GMP is unofficial and should not be used as an investment basis.

What are the Alpine Texworld IPO dates and price band? The IPO runs from July 14 to July 16, 2026, at a price band of ₹100–₹105 per share, with listing expected on July 21, 2026 on the NSE and BSE.

What is the lot size and minimum investment? The lot size is 142 shares, requiring a minimum retail investment of ₹14,910 at the upper price band.

Is the Alpine Texworld IPO worth applying to? For listing-gain investors, the weak subscription (0.48x on Day 2), aggressive valuation, and a CRISIL downgrade to BB/Stable make it a high-risk bet best approached with caution or skipped. Long-term investors convinced by the business should read the RHP carefully first.

What does Alpine Texworld do? It manufactures and processes fabrics and yarn — including denim, suiting, shirting and RFD fabrics — and runs captive solar power plants to reduce energy costs.

Related Reading

Gold Rate Today in India — Live 24K, 22K, 18K Prices: https://www.gpaisa.in/gold-rate

Silver Rate Today in India — Live Prices: https://www.gpaisa.in/silver-rate

All Commodity Prices: https://www.gpaisa.in/commodities

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Grey market premium figures are unofficial and not regulated by SEBI. IPO investments are subject to market risks. Investors should read the Red Herring Prospectus carefully and consult a SEBI-registered financial advisor before investing.