Sukanya Samriddhi Yojana (SSY) 2026: 8.2% Interest Rate, Calculator & Complete Guide for Parents

By Satyapal Khakhal, Personal Finance Writer | Last Updated: 12 June 2026

SSY interest rate data from Ministry of Finance notification dated March 30, 2026 (Q1 FY2026-27). Scheme rules from India Post official documentation and National Savings Institute guidelines. Tax provisions from Income Tax Act as applicable for FY 2026-27. All maturity calculations are illustrative based on current 8.2% rate held constant — actual maturity amount depends on quarterly rate revisions. gpaisa.in is not registered with SEBI.

When my neighbour's daughter was born last year, the first financial decision he made was not about health insurance or a child plan. He walked to the nearest post office and opened a Sukanya Samriddhi Yojana account. He deposited ₹5,000 that day. He will deposit every month for the next 15 years.

By the time his daughter turns 21, that account will hold approximately ₹27 lakh — completely tax-free, guaranteed by the Government of India, earning a rate that no bank FD currently offers to retail investors.

This is what SSY does. It is not a complex financial product. It is a government-backed promise to help parents of daughters build a meaningful corpus for their child's education and future — with the best interest rate available on any guaranteed savings scheme in India today.

This guide covers everything you need to know — current interest rate, what your investment actually grows to, the rules that matter, and how to open an account today.

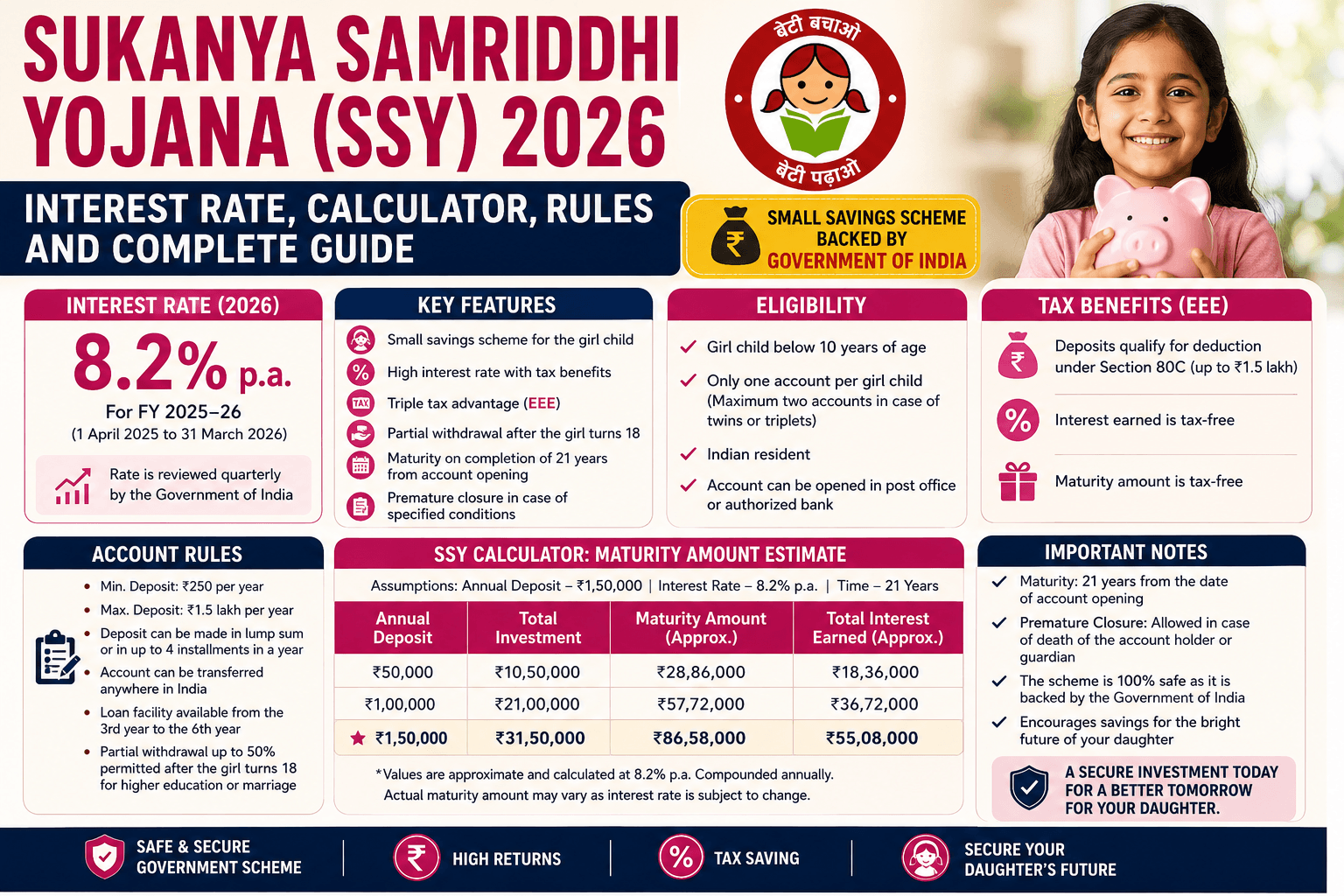

SSY Interest Rate — June 2026: Confirmed at 8.2%

The Ministry of Finance confirmed on March 30, 2026 that the Sukanya Samriddhi Yojana interest rate for Q1 FY2026-27 (April–June 2026) remains unchanged at 8.2% per annum, compounded annually.

This is the 8th consecutive quarter at 8.2% — the rate has not changed since January 2024. The rate is reviewed quarterly and set by the government based on government security yields. Historical SSY rates:

| Period | SSY rate | PPF rate | SSY advantage |

|---|---|---|---|

| April–June 2026 | 8.2% | 7.1% | +1.1% |

| January–March 2026 | 8.2% | 7.1% | +1.1% |

| April 2024–March 2026 | 8.2% | 7.1% | +1.1% |

| July 2023–December 2023 | 8.0% | 7.1% | +0.9% |

| April 2020–June 2023 | 7.6% | 7.1% | +0.5% |

| March 2020 (COVID cut) | 7.6% | 7.1% | +0.5% |

| 2018–2019 (peak) | 8.5% | 8.0% | +0.5% |

Source: Ministry of Finance quarterly notifications. SSY has consistently offered 0.5–1.1% higher rate than PPF across its entire history since 2015.

At 8.2%, SSY currently offers a higher guaranteed rate than SBI FD (6.25%), HDFC FD (6.50%), Post Office 5-year TD (7.50%), and PPF (7.1%). For a parent of a daughter, this is the single best guaranteed return available in India today — and every rupee earned is completely tax-free.

SSY at a Glance: Key Facts

| Feature | Details |

|---|---|

| Interest rate (April–June 2026) | 8.2% p.a., compounded annually |

| Tax status | EEE — completely tax-free (investment, interest, maturity) |

| Minimum annual deposit | ₹250/year |

| Maximum annual deposit | ₹1,50,000/year |

| Deposit period | 15 years from account opening |

| Maturity period | 21 years from account opening |

| Account opening eligibility | Girl child from birth to 10 years of age |

| Who can open | Natural parents or legal guardian only |

| Maximum accounts per family | 2 accounts (one per daughter); 3 if twins/triplets |

| Partial withdrawal | 50% of previous year-end balance after daughter turns 18 |

| Premature closure | Only on marriage after 18, or death, or extreme compassionate grounds |

| Where to open | All India Post offices, SBI, HDFC, ICICI, Axis, Kotak, and most scheduled banks |

| Backed by | Government of India — sovereign guarantee |

SSY Calculator: What Your Monthly Investment Actually Grows To

The most important question every parent asks: if I invest ₹X every month, how much will my daughter have at 21? Here are the real numbers at the current 8.2% rate, assuming deposits for 15 years and then the account continues for 6 more years without new deposits:

| Monthly deposit | Annual deposit | Total invested (15 years) | Maturity corpus (21 years) | Tax-free gain |

|---|---|---|---|---|

| ₹1,000/month | ₹12,000 | ₹1,80,000 | ~₹5.3 lakh | ₹3.5 lakh |

| ₹2,000/month | ₹24,000 | ₹3,60,000 | ~₹10.6 lakh | ₹7.0 lakh |

| ₹3,000/month | ₹36,000 | ₹5,40,000 | ~₹15.9 lakh | ₹10.5 lakh |

| ₹5,000/month | ₹60,000 | ₹9,00,000 | ~₹26.5 lakh | ₹17.5 lakh |

| ₹8,000/month | ₹96,000 | ₹14,40,000 | ~₹42.4 lakh | ₹28.0 lakh |

| ₹10,000/month | ₹1,20,000 | ₹18,00,000 | ~₹53.0 lakh | ₹35.0 lakh |

| ₹12,500/month | ₹1,50,000 | ₹22,50,000 | ~₹66.2 lakh | ₹43.7 lakh |

Calculations assume 8.2% rate held constant throughout. Actual maturity depends on quarterly rate revisions. Deposits made on the 1st of each month. Annual compounding applied. These are illustrative — use a detailed SSY calculator for exact figures.

The power of SSY is visible in that last row: ₹12,500/month (₹1.5 lakh/year — the maximum) invested for 15 years grows to ₹66.2 lakh. Total invested: ₹22.5 lakh. Tax-free gain: ₹43.7 lakh. The government-guaranteed interest earns nearly twice what you put in — and the entire ₹66.2 lakh comes out completely tax-free.

At 8.2%, SSY beats PPF (7.1%) by enough to matter significantly over a 21-year period. The same ₹12,500/month in PPF at 7.1% would yield approximately ₹54.3 lakh — ₹11.9 lakh less than SSY, on identical deposits. SSY's 1.1% rate advantage over PPF adds ₹11.9 lakh to your daughter's corpus on maximum deposits.

The Tax Benefit: EEE Status Explained

SSY has EEE tax status — meaning the investment is exempt, the interest earned is exempt, and the maturity proceeds are exempt from income tax. This is the same triple exemption as PPF, making SSY one of only a handful of instruments in India with this status.

Section 80C deduction: Deposits up to ₹1.5 lakh per year qualify for Section 80C deduction — but only under the old tax regime. Under the new tax regime (default from FY 2024-25), Section 80C deductions are not available. However, even without the 80C deduction, SSY's interest and maturity proceeds remain completely tax-free regardless of which tax regime you use. The EEE status is not dependent on the 80C deduction — it is a fundamental feature of the scheme.

For a parent in the 30% tax bracket on the old regime: The ₹1.5 lakh annual deduction saves ₹46,800 in tax every year. Over 15 years of deposits — ₹7,02,000 in total tax saved on the investment alone, before accounting for the tax-free interest and maturity.

For a parent on the new tax regime: No 80C deduction, but the interest (compounding at 8.2%) and the entire ₹66.2 lakh maturity amount remain tax-free. Compared to a taxable FD at the same 8.2% rate (hypothetical), a 30% bracket parent would save approximately ₹13-14 lakh in tax on the interest alone over the 21-year period.

SSY Rules Every Parent Must Know

Rule 1: Account must be opened before daughter's 10th birthday

This is the most critical eligibility condition. SSY accounts can only be opened for girls who have not yet turned 10. There is no exception. A girl who turns 10 tomorrow is permanently ineligible — the account cannot be opened the day after her birthday. Parents of older daughters cannot retroactively open SSY accounts. If you have a daughter under 10, open the account as soon as possible — even with ₹250 to activate it.

Rule 2: Minimum deposit ₹250/year — not ₹250 total

You must deposit a minimum of ₹250 in every financial year. If you miss a year's minimum deposit, the account becomes a "default account." To regularise it, pay a penalty of ₹50 per defaulted year plus the minimum ₹250. The account continues to earn interest even during default periods, but it cannot be used for partial withdrawal until regularised.

Rule 3: Deposits are required for 15 years only

Many parents mistakenly believe they must deposit for 21 years. You only need to deposit for the first 15 years from account opening. After year 15, no new deposits are required or accepted — the account earns interest on the accumulated balance for the remaining 6 years and matures at the end of year 21. The 6-year compounding period after deposits stop is when the corpus grows most rapidly.

Rule 4: Partial withdrawal for education — rules are strict

50% of the balance at the end of the previous financial year can be withdrawn for higher education after the daughter turns 18. This is not automatic — you must provide proof of admission to a recognised institution (university admission letter or fee demand notice). The withdrawal can be taken as a lump sum or in up to 5 annual instalments. It cannot be used for any purpose other than education — withdrawal for other reasons is not permitted without closing the account.

Rule 5: Account matures in two ways

The SSY account matures either 21 years from the date of opening, OR on the daughter's marriage after she turns 18 — whichever comes first. If the account is closed for marriage, it must be closed within one month before or three months after the marriage date with supporting documents. The full balance (including interest) is paid out tax-free.

Rule 6: NRI status invalidates the account

If the account holder's family acquires NRI status after opening an SSY account, the account must be closed. From the date of NRI status, the interest rate reverts to the Post Office Savings Account rate (currently 4%) rather than 8.2%. This is a significant consideration for parents who may be planning to work abroad — the 8.2% rate is available only for Indian residents.

Rule 7: Grandparents cannot open the account

SSY accounts can only be opened by natural parents or court-appointed legal guardians. Grandparents — even when they are the primary caregivers — cannot open SSY accounts unless they have formal legal guardianship. This is a frequently misunderstood rule that causes frustration at post office branches.

SSY vs PPF vs FD: Which is Better for Your Daughter's Future?

| Feature | SSY | PPF | Bank FD (5yr Tax Saving) |

|---|---|---|---|

| Current rate | 8.2% | 7.1% | 6.25%–7.50% |

| Tax on interest | Tax-free | Tax-free | Taxed at slab rate |

| Tax on maturity | Tax-free | Tax-free | Taxed |

| 80C deduction | Yes (old regime) | Yes (old regime) | Yes (old regime) |

| Lock-in period | 21 years (partial from age 18) | 15 years (partial from year 7) | 5 years (no withdrawal) |

| Who can invest | Parents of daughters only | Anyone | Anyone |

| Sovereign guarantee | Yes | Yes | DICGC up to ₹5 lakh |

| Maturity on ₹1.5L/year × 15 years | ~₹66.2 lakh (tax-free) | ~₹54.3 lakh (tax-free) | ~₹11.3 lakh (taxable) |

The comparison is clear: for parents of daughters with a 21-year horizon, SSY is strictly better than PPF on rate, better than FD on both rate and tax treatment. If you have a daughter under 10 and are currently investing for her future in PPF or FDs — switch the daughter-specific allocation to SSY. Keep PPF for your own retirement corpus.

How to Open a Sukanya Samriddhi Yojana Account in 2026

Step 1 — Choose where to open

SSY accounts are available at all India Post offices and at most scheduled banks including SBI, HDFC, ICICI, Axis, Kotak, PNB, and Bank of Baroda. Post offices typically have faster processing. HDFC and SBI offer online tracking through their net banking portals once the account is opened.

Step 2 — Gather documents

You will need the following:

- Girl child's birth certificate (original + photocopy)

- Parent/guardian's identity proof — Aadhaar card (preferred), PAN card, or passport

- Parent/guardian's address proof — Aadhaar, voter ID, utility bill, or bank statement

- Passport-size photographs of parent/guardian (2 copies)

- SSY account opening form (Form-1) — available at post offices and bank branches, or downloadable from India Post website

Step 3 — Fill the application form

Form-1 requires: girl child's name and date of birth, parent/guardian's name and relationship, nominee details, and the initial deposit amount. The form is straightforward — most post office staff will help you fill it.

Step 4 — Make the initial deposit

The minimum initial deposit is ₹250. You can deposit up to ₹1,50,000 in the first year. Cash, cheque, and demand draft are accepted. At most banks, net banking transfer is also accepted for subsequent deposits.

Step 5 — Receive passbook

After account opening, you receive a passbook showing the account number, opening date, and initial deposit. Keep this safely — it is the primary record of your account. The passbook must be presented for all withdrawals and at maturity.

Online SSY account opening: HDFC Bank, Axis Bank, and India Post Payments Bank allow SSY account opening online for existing customers. The process involves uploading documents and completing KYC digitally — no branch visit required for these banks. Verify availability on your bank's official website.

Smart SSY Investment Strategies

Deposit before April 5 each year for maximum interest:

SSY interest is calculated on the lowest balance between the 1st and 5th of each calendar month. If you deposit before the 5th, that month's balance earns interest. If you deposit after the 5th, that deposit earns no interest for that month. Depositing your annual ₹1.5 lakh in one payment on April 1 or 2 earns a full year of interest on the entire amount — maximising your return.

Open early — every year matters:

Opening the account on the day of birth versus waiting until age 5 makes a significant difference. A child whose account is opened at birth gets 21 years of compounding; one opened at age 5 gets only 16 years. At ₹1.5 lakh/year, that 5-year difference is approximately ₹14–15 lakh in maturity corpus. The earliest possible opening date is the optimal financial decision.

For two daughters — open two accounts:

Each daughter is entitled to one SSY account. Two daughters means two accounts, each with the full ₹1.5 lakh annual limit. Total family SSY investment: ₹3 lakh/year (₹25,000/month). At maximum deposits across both accounts, both daughters have ₹66.2 lakh at maturity each — completely tax-free.

SSY + term insurance combination:

SSY guarantees your daughter's corpus only if you are alive to make deposits. If you pass away before the deposit period ends, your nominee will receive whatever is in the account. Pair your SSY with a term insurance policy of sufficient cover — so that even in your absence, the corpus can be continued. A ₹1 crore term plan with the SSY creates a complete financial security structure for your daughter.

Common Mistakes Parents Make with SSY

Waiting to open the account: "She is only 2, I will open it when she is 5" is a commonly heard reason. Every year of delay is a year of 8.2% compounding lost. At ₹5,000/month, opening at birth vs age 5 costs approximately ₹5–6 lakh in final corpus.

Depositing in December instead of April: Depositing the annual amount in December instead of April means 8 months of interest is missed on that deposit. At ₹1.5 lakh annual deposit, this costs approximately ₹8,200 per year — ₹1.23 lakh over 15 years — purely from timing.

Using SSY for non-education expenses after age 18: The 50% partial withdrawal is only for higher education. Many parents discover this rule only when they want to use the funds for something else at age 18. Plan accordingly — if you anticipate needing the funds for non-education purposes, maintain a separate savings vehicle alongside SSY.

Treating SSY as a marriage corpus: SSY is often opened with marriage as the goal. This is fine, but the 21-year maturity means a daughter born today will access the full corpus at age 21 — which may or may not align with your marriage timeline. If marriage is the primary goal and you want more flexibility on timing, supplement SSY with a separate flexible investment.

What Happens at Maturity

When the SSY account matures — 21 years from opening — the entire corpus is paid out to the daughter (not the parent). She must be at least 18 years old to receive the maturity amount. If she is below 18 at the 21-year mark (which cannot happen if the account was opened at birth, since 21 years from birth = age 21 — but could happen with late opening for a very young child), the guardian manages the account until she turns 18.

For maturity withdrawal, she needs to submit the passbook, identity proof, address proof, and a withdrawal request form at the post office or bank branch. The amount is transferred to her bank account — the entire corpus including all accumulated interest, completely tax-free.

Frequently Asked Questions

What is the current Sukanya Samriddhi Yojana interest rate in 2026?

8.2% per annum, compounded annually — confirmed for Q1 FY2026-27 (April–June 2026) by the Ministry of Finance notification dated March 30, 2026. This rate has been unchanged for 8 consecutive quarters since January 2024. It is the highest rate among all small savings schemes in India.

If I invest ₹5,000/month in SSY, how much will I get at maturity?

At 8.2% held constant, ₹5,000/month (₹60,000/year) for 15 years gives approximately ₹26.5 lakh at 21-year maturity. Total invested: ₹9 lakh. Tax-free gain: ₹17.5 lakh. The entire ₹26.5 lakh is tax-free.

Can I open an SSY account online?

HDFC Bank, Axis Bank, and India Post Payments Bank offer online SSY account opening for existing customers. For other banks and post offices, a branch visit is required. Subsequent deposits can be made online through most banks' net banking portals after the initial physical account opening.

What happens to SSY if I become NRI after opening the account?

The account must be closed. From the date of NRI status, interest reverts to the Post Office Savings Account rate (4%) instead of 8.2%. If you are planning to work abroad, factor this in before making large SSY commitments — the account only earns the full 8.2% for Indian residents.

Can I have both PPF and SSY accounts simultaneously?

Yes — absolutely. PPF is for your own retirement corpus. SSY is for your daughter's future. Both can (and should) be maintained simultaneously. They serve different goals and the ₹1.5 lakh annual limit applies separately to each. SSY's 8.2% rate makes it superior to PPF for the daughter-specific allocation.

What is the penalty for not depositing in a year?

The account becomes a "default account" and earns a penalty of ₹50 per defaulted year, plus the minimum ₹250 must be deposited to regularise. The account continues to earn 8.2% interest during the default period. There is no other punishment — the account does not close, and all accumulated interest is retained.

Can my daughter withdraw from SSY before maturity for purposes other than education?

No. The partial withdrawal after age 18 is specifically for higher education expenses — admission fees, tuition, hostel. It cannot be used for marriage, personal expenses, or any other purpose without closing the account. Full premature closure is permitted only for marriage after age 18, death of the account holder, or extreme compassionate grounds approved by the government.

Use our calculators: PPF Calculator | FD Calculator | SIP Calculator

Related reading: PPF vs ELSS vs FD — Best 80C Investment 2026 | How to Improve Your CIBIL Score | Best FD Rates June 2026

Disclaimer: SSY interest rates are reviewed quarterly by the Ministry of Finance and can change. All maturity calculations in this article are illustrative based on the current 8.2% rate held constant — actual corpus depends on future rate revisions. This article is for informational and educational purposes only and does not constitute financial advice. Please verify all scheme details at your nearest post office or India Post official website before investing. gpaisa.in is not registered with SEBI.