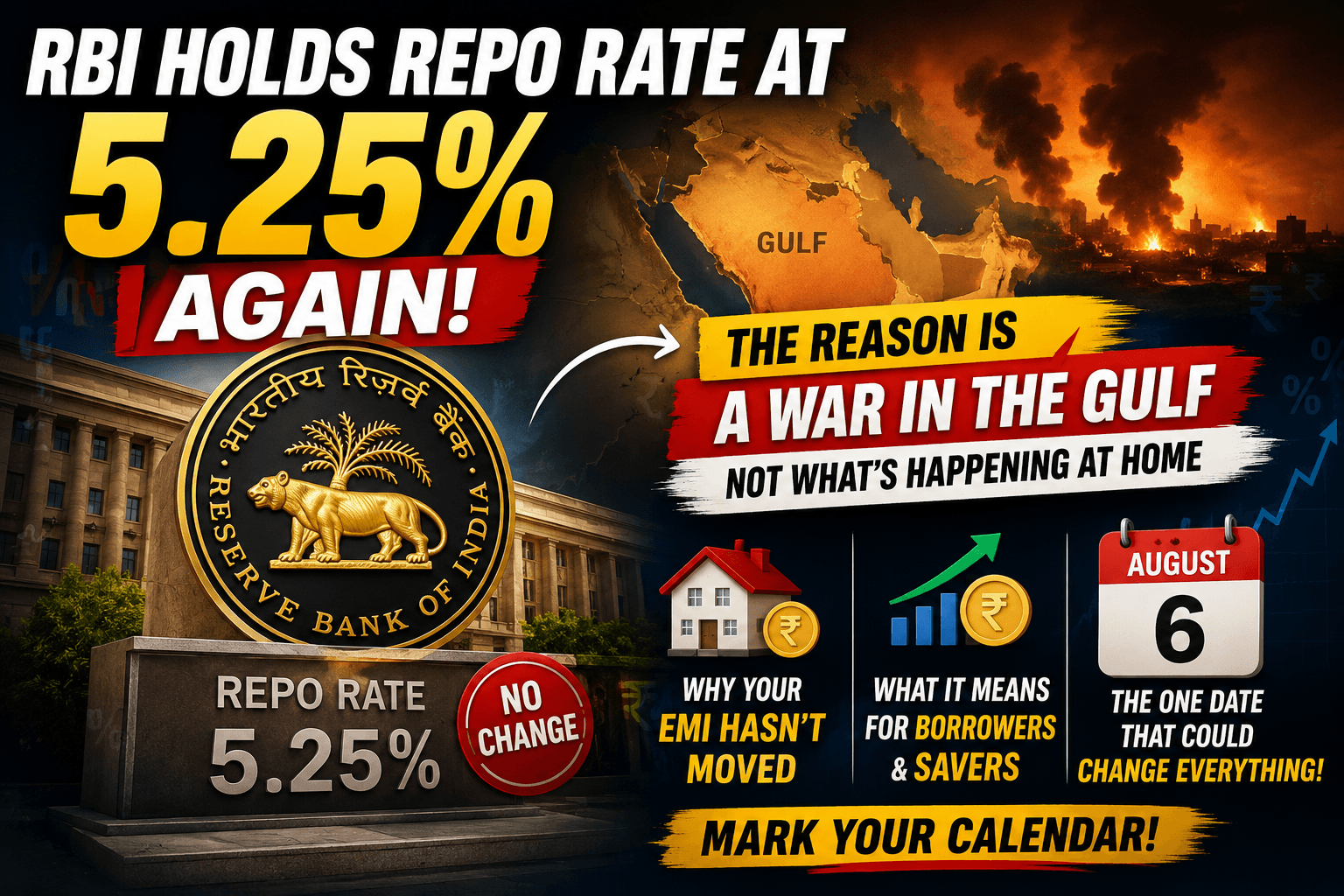

RBI Repo Rate News: Why the Rate Is Still Stuck at 5.25% — and What August Could Change

By Satyapal Khakhal

If you've been waiting for your home loan EMI to drop, here's the short version: it hasn't moved, and it probably won't until the RBI's next big meeting in August. But the why behind that pause is where the real story is — and it has a lot more to do with a war in the Gulf than with anything happening in Mumbai.

Let me break down what's actually going on, in plain language.

The headline: rate held at 5.25%

At its last Monetary Policy Committee (MPC) meeting on June 5, 2026, the Reserve Bank of India kept the repo rate unchanged at 5.25%. All six members of the committee voted for the hold — a clean 6-0. The stance stayed "neutral."

The repo rate, if you're rusty on the jargon, is simply the rate at which the RBI lends to commercial banks. It's the anchor for almost everything else: your floating home loan, your car loan, the interest your bank pays on deposits. When it moves, your EMI eventually moves with it. When it sits still — as it is now — so does your EMI.

The supporting rates didn't budge either: the Standing Deposit Facility stays at 5.00% and the Marginal Standing Facility and Bank Rate remain at 5.50%.

So why did the RBI hit pause?

Here's the part most headlines skip. The RBI actually started cutting rates back in December 2025, and borrowers were hoping that cycle would keep going through 2026. Then the Gulf changed the math.

The escalating conflict in West Asia and the disruption around the Strait of Hormuz have pushed crude oil prices sharply higher. For a country that imports the vast majority of its oil, that's a direct hit to inflation. Cutting rates into rising inflation would be like pressing the accelerator and the brake at the same time — so the RBI chose to wait.

Governor Sanjay Malhotra was blunt about the risk, pointing to persistently elevated energy prices and the possibility of El Niño conditions as real threats to the inflation outlook. In other words: too much uncertainty to make a move right now.

The numbers that tell the real story

The rate staying flat is almost the least interesting thing about the June policy. The forecasts that came with it are what matter:

Growth got downgraded. The RBI cut its GDP growth forecast for FY2026-27 to 6.6%, down from an earlier 6.9%. That signals the central bank sees genuine headwinds for the economy — especially for businesses exposed to energy and logistics costs.

Inflation got upgraded — the wrong way. The inflation projection was raised to an average of 5.1%, up from 4.6%, driven by higher LPG, base metal, plastic, and rubber prices. Later quarters could see inflation near 5.9%.

Put those two together — slower growth and higher inflation — and you get the classic central-banker's dilemma. It's the exact situation where cutting rates is dangerous and hiking rates would choke growth. So the RBI does the only sensible thing: it waits and watches.

What this means for you, specifically

If you have a home loan or any floating-rate loan: no relief yet. Your EMI stays where it is. If you were banking on a mid-year cut to ease your budget, that plan needs to move to the second half of the year — at the earliest.

If you're a saver or retiree: this is quietly good news. A pause means fixed deposit rates stay attractive for longer. If you've been meaning to lock into an FD, the current window is a reasonable one, because once rate cuts resume, deposit rates typically fall.

If you're an equity investor: an expected hold is a non-event for markets — it was already priced in. The growth downgrade matters more. Companies with heavy fuel or freight exposure are the ones to watch for margin pressure.

If you're planning to borrow soon: don't wait around hoping for a cut before August. Base your decision on your own finances, not on a rate move that may or may not come.

The one date that matters now: August 3–5

The next MPC meeting runs from August 3 to 5, 2026, and it's shaping up to be the real decision point. What happens there hinges almost entirely on things outside the RBI's control:

Crude oil and the Gulf. This is the big one. If there's a ceasefire and the Strait of Hormuz reopens, oil prices could fall quickly, inflation pressure would ease, and the RBI would suddenly have room to resume cutting rates. If the conflict drags on, expect the pause to continue.

The June and July inflation prints. If core inflation starts creeping up alongside energy prices, the RBI's job gets much harder.

The monsoon. A weak monsoon would stack food inflation on top of energy inflation — another reason to stay on hold.

The bottom line

The RBI isn't sitting still because nothing is happening. It's sitting still because too much is happening — a war-driven oil spike, an uncertain monsoon, and an economy that's slowing just as prices are rising. Holding at 5.25% is the RBI buying itself time to see which way the risks break.

For now, the message to borrowers is patience, and the message to savers is opportunity. Everything after that runs through what happens in August — and, honestly, through what happens in the Gulf.

Related reading:

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Policy rates and forecasts are subject to change based on RBI decisions. Please consult a SEBI-registered financial advisor before making borrowing or investment decisions.