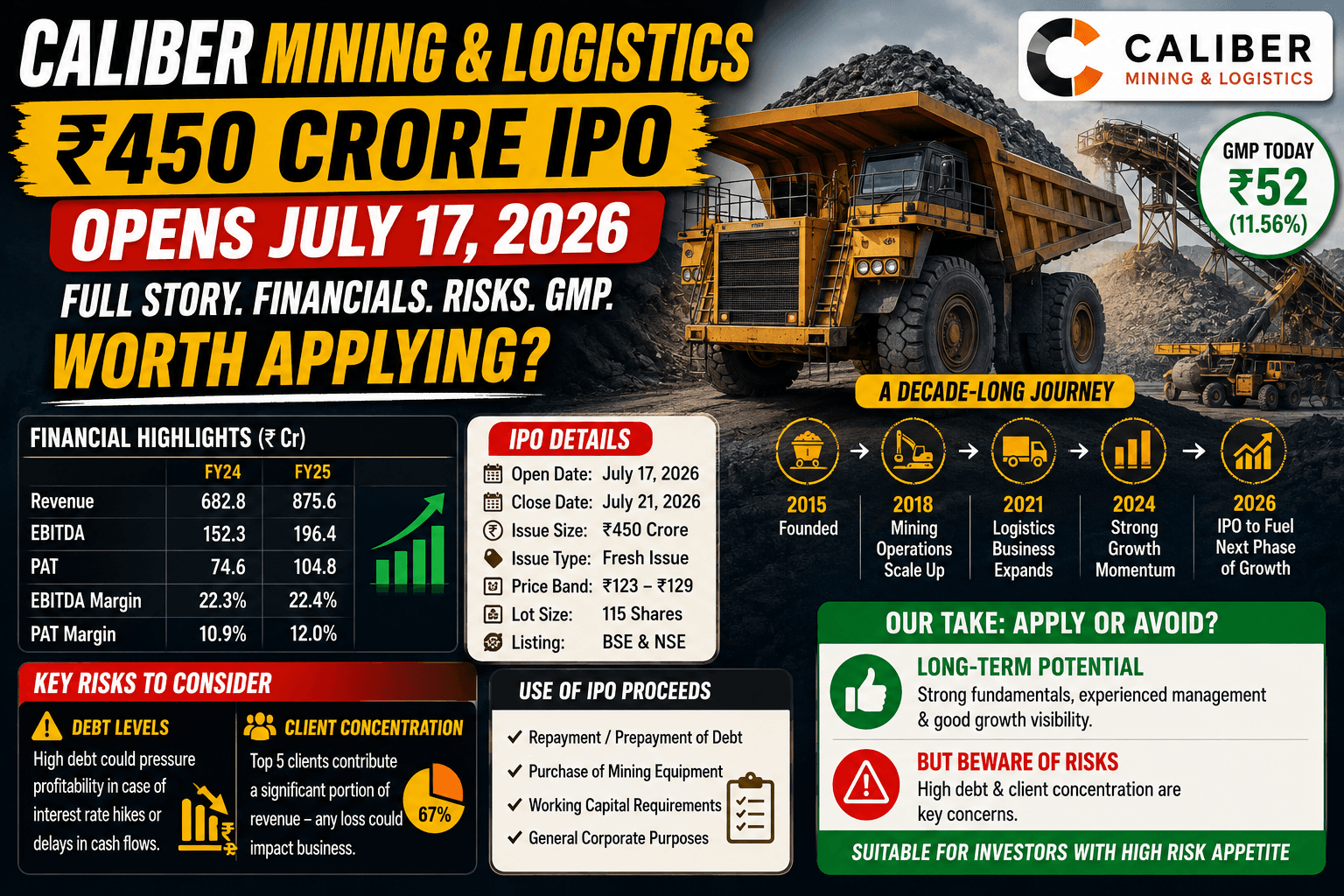

Caliber Mining and Logistics IPO 2026: Full Review, Company History, Financials & Honest Insight

By Satyapal Khakhal

Every so often an IPO comes along that isn't a household name but quietly runs a serious business behind the scenes. Caliber Mining and Logistics is one of those. You've probably never heard of it — yet the coal that powers a chunk of India's electricity has, at some point, been dug up or hauled by this Chandrapur-based company. Here's a complete, no-hype breakdown of the IPO, the company's story, its numbers, and the real risks worth knowing before you apply.

Caliber Mining and Logistics IPO: Key Details at a Glance

The IPO opens on Friday, July 17, 2026 and closes on Tuesday, July 21, 2026. The price band is set at ₹402 to ₹424 per share, with a face value of ₹10. The lot size is 35 shares, so the minimum retail investment at the upper band works out to ₹14,840.

This is a mainboard IPO aiming to raise ₹450 crore in total, split between a fresh issue of ₹400 crore (94,33,962 shares) and an offer for sale of ₹50 crore (11,79,245 shares) from promoters. Shares are expected to list on both the BSE and NSE on July 24, 2026, with allotment likely finalised on July 22. DAM Capital Advisors is the book-running lead manager, and KFin Technologies is the registrar.

At the upper price band, the company commands a market capitalisation of roughly ₹2,772 crore.

Where the Money Goes

Unlike a pure offer-for-sale, most of this issue brings fresh capital into the company. Of the ₹400 crore fresh issue, around ₹208 crore is earmarked for repaying or prepaying borrowings, and about ₹167 crore for buying machinery — dump trucks, an excavator, a bulldozer and a grader, among other equipment. The rest goes to general corporate purposes. The ₹50 crore OFS portion goes to selling promoters, not the company.

That debt-repayment focus matters, and we'll come back to why.

Company History: From "Mercantile" to Mining Muscle

Caliber's story is a lesson in reinvention. The company was originally incorporated in July 2014 as Caliber Mercantile Private Limited — a name that gives away nothing about coal. Over the following decade it built itself into a full-fledged mining-support and logistics operator, and the paperwork finally caught up in 2024: it became Caliber Mining and Logistics Private Limited in July 2024, then converted to a public limited company that September ahead of its IPO plans.

Today, headquartered in the coal belt of Chandrapur, Maharashtra, Caliber is what the industry calls an integrated service provider for the coal sector. In plain terms, it does the heavy, unglamorous work that turns a coal deposit into delivered fuel: removing the overburden (the soil and rock sitting on top of a coal seam), extracting the coal, loading and unloading it, and then moving it by road and coordinating rail transport. It's a genuine one-stop shop, and that end-to-end model is its main selling point.

The company operates across Maharashtra, Madhya Pradesh and Chhattisgarh, running operations at around 10 mines — though, importantly, it doesn't own any of those mines. Its biggest customers are two subsidiaries of Coal India: Western Coalfields (WCL) and Northern Coalfields (NCL). To deliver all this, Caliber runs a large fleet — roughly 1,911 vehicles and machines as of April 30, 2026, including hundreds of tippers, excavators, loaders and tip trailers — and employs over 5,500 people. The promoter family, the Chaddas, run the show, with Mohit Satishkumar Chadda as Chairman and Managing Director. Notably, a former Chairman of Coal India sits on the board as an Independent Director — a useful signal of sector credibility given how concentrated the client base is.

The company has also started diversifying: it moved into iron ore logistics in FY2023, an early attempt to reduce its reliance on coal alone.

Financial Performance: Fast Growth, Funded by Debt

The growth here is real and impressive. Over the past four years, revenue has compounded at around 46% a year, climbing from about ₹372 crore in FY22 to roughly ₹1,678 crore in FY26. Looking at the more recent numbers:

Total income: ₹957.9 crore (FY24) → ₹1,435.6 crore (FY25) → ₹1,684.7 crore (FY26)

Profit after tax (PAT): ₹95.9 crore (FY24) → ₹131.6 crore (FY25) → ₹157.9 crore (FY26)

EBITDA: ₹243.1 crore (FY24) → ₹349.8 crore (FY25) → ₹430.9 crore (FY26)

That gives FY26 an EBITDA margin of about 25.6% and a net margin near 9.4% — healthy for a contract-based mining services business. Return on equity for FY26 was a strong ~28%. Working capital is well managed too, with receivables collected in roughly a month despite serving government-sector clients, who are not always quick to pay.

The order book tells the growth story going forward: it stood at a substantial ₹9,550 crore as of May 15, 2026, up sharply from ₹5,668 crore at the end of March — giving multi-year revenue visibility.

The Insight: What the Headline Numbers Don't Show

Here's where you need to look past the glossy growth figures.

The growth has been bought with debt. Caliber's expansion has been capex-led — it added roughly ₹1,470 crore of gross block over four years — and that was funded heavily by borrowing. Total debt stood at around ₹1,146 crore as of April 30, 2026, up from ₹1,058 crore in March. That's a pre-IPO net debt-to-equity ratio near 1.5:1, which is on the high side. This is precisely why ₹208 crore of the fresh issue is going to debt repayment. Post-IPO, that ratio should nearly halve to around 0.8:1 — better, but still not light. Its long-term borrowings carry a CRISIL rating of BBB+/Stable.

Client concentration is the real risk. Nearly all of Caliber's revenue comes from just two Coal India subsidiaries. If a contract isn't renewed, or pricing terms tighten, the impact would be immediate and large. The presence of a former Coal India chairman on the board softens this somewhat, but it doesn't eliminate it.

It doesn't own the mines. Because Caliber operates on contracts at mines it doesn't own, any delay in the mine owner's approvals, licences or permits can halt work at a site. Add the everyday hazards of open-pit operations — flooding, equipment breakdowns, diesel or water shortages — and you have a business with real operational sensitivity.

On valuation, the pricing looks fair rather than cheap. At the upper band, the issue is priced at a post-IPO P/E of about 17.5x and a price-to-book of roughly 7.3x. On forward FY27 estimates, however, analysts peg the P/E closer to 12.8x and EV/EBITDA around 7.5x — which looks reasonable given the historic growth. One useful anchor: the company raised primary capital at ₹240 per share in late 2024, so the IPO price of ₹424 is about a 77% premium in under two years — broadly in line with how fast its EBITDA has grown over the same period. As equity expands post-IPO, that stellar ~28% RoE will likely settle around 20% in the next couple of years.

Grey Market Premium (GMP)

Ahead of the opening, Caliber's IPO was quoting a grey market premium of around ₹80 on July 15, implying an estimated listing gain of roughly 19% over the ₹424 upper band — a sign of healthy but not frenzied interest.

A necessary reality check: GMP is an unofficial, unregulated indicator that swings daily with sentiment and has no bearing on the actual listing price. Some analysts refuse to quote it at all, viewing it as against the spirit of SEBI norms. Treat it as a mood reading, never as a forecast, and never as a reason to invest.

Strengths and Risks: The Balanced View

Strengths: a genuinely integrated coal mining-and-logistics model; a strong, multi-year order book of over ₹9,500 crore; impressive revenue and profit growth with healthy margins; deep relationships with Coal India subsidiaries; experienced promoters and credible board representation; and disciplined working-capital management.

Risks: high dependence on just two clients; elevated debt even after repayment; no ownership of the mines it operates; exposure to open-pit operational hazards; and a valuation that already prices in much of the good news, leaving less margin for error.

Should You Apply?

Caliber Mining and Logistics is a fundamentally sound, fast-growing company in an unglamorous but essential corner of India's energy supply chain. The fresh-capital focus on cutting debt is a genuine positive, and the order book offers rare visibility. The counterweights are equally clear: heavy client concentration and a still-leveraged balance sheet.

On balance, this looks like an issue better suited to investors with a medium-to-long-term horizon who are comfortable with the coal sector's structural questions and the company's single-client dependency — rather than those chasing a quick listing pop. As always, read the RHP, weigh the risks against your own goals, and don't let grey market chatter make the decision for you.

Related reading:

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Grey market premium figures are unofficial and not regulated by SEBI. IPO investments are subject to market risks. Investors should read the Red Herring Prospectus carefully and consult a SEBI-registered financial advisor before investing.